of coal per man-shift in opencast and

underground mines, respectively,

which pales in comparison to Australia

where opencast coal and underground

mining production per man-shift

amounted to 74 t and 40 t, respectively.

Coal India’s machines also work

15 hr/day, compared with 22 hr/day in

Australia.

Brakes on growth to

remain

Barring any announcements of capital

injections and major increases in

CAPEX, BMI is reluctant to further

upgrade its already optimistic

forecasts of annual average growth of

7.4% in 2016 – 2019.

Although it is possible for

Coal India to hit its production targets

by sustaining annual average

production growth of 13.4% during

2016 – 2020, four key obstacles remain,

besides improving productivity and

production:

n

n

The opening of new mines could

remain hampered if environmental

clearances are not made in

an expedient manner. As of

August 2014, Coal India had 48

mines awaiting environmental

clearances. It currently has close to

500 mines in operation.

n

n

Coal India might not be able

to construct sufficient railway

infrastructure by 2020 to

improve offtake, which would

limit efforts to open mines that

could add about 300 milion tpa

of coal production from the

states of Odisha, Jharkhand and

Chhattisgarh.

n

n

Given India’s insistence on not

exceeding its targeted budget

deficit, the government will need

to come up with an innovative

workaround to finance the

purchase of new freight trains

by India Railways in order to

transport the coal, other than

raising railway fares, as the cost

of railway travel is an extremely

sensitive issue to the public.

n

n

The threat of strikes by mining

unions could derail efforts to

improve productivity. Given that

Coal India produces approximately

80% of India’s coal, by going

on strike the coal unions could

plunge the entire country into

darkness. Given the opposition

faced by the government when it

wanted to privatise a small stake

of Coal India in the past year,

the threat of renewed strikes by

union workers poses downside

risks on Coal India’s ability to

raise further capital from equity

markets to fund major upgrades

in equipment. India’s efforts to

introduce competition to the

de facto monopoly by allowing

foreign private players might

result in long-lasting strikes, which

could significantly reduce the

company’s operating performance

and stymie its efforts to raise

productive capacity by acquiring

more modern equipment.

Imports to remain strong

– for now

Coal imports will remain strong over

the coming quarters as India will

continue to be unable to meet domestic

coal consumption. Even though

domestic coal production is rising

faster than domestic consumption,

seaborne coal demand from power

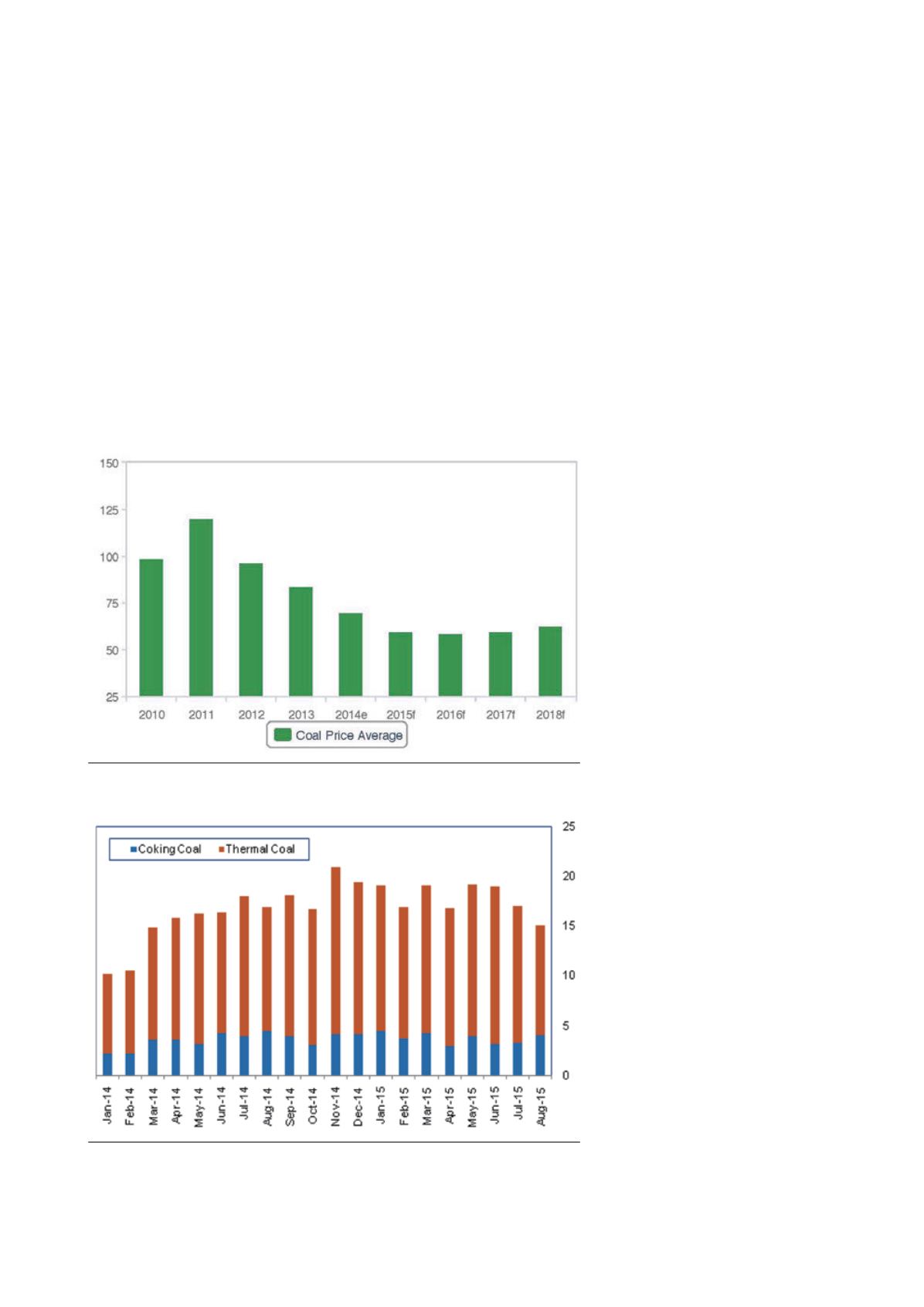

Prices to remain relatively low: Newcastle thermal coal (US$/t).

Source: BMI, Bloomberg.

Coal imports to remain elevated: India – thermal and metallurgical coal imports

(million t).

Source: BMI, Bloomberg.

16

|

World Coal

|

January 2016